Volatility Cycle

December 2, 2016, 8:55 AM

Indicators

0 Comments

{kind=link}

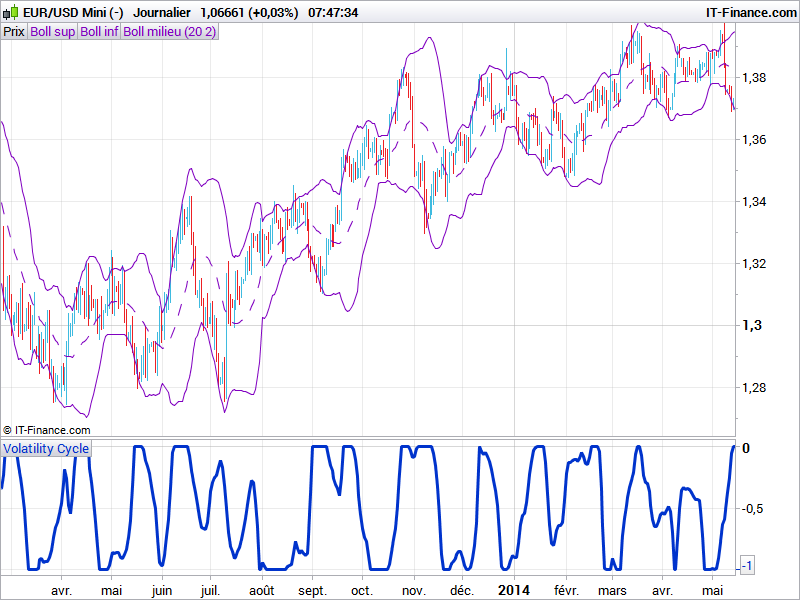

The volatility cycle indicator measure differences between current standard deviation of the price and its highest and lowest within the last “InpBandsPeriod” bars. It results of a bounded oscillator that can be read as:

- oscillator is low, expect a volatility explosion in the next periods or the end of the current trend

- oscillator is high, a trend is currently forming

The curve can be smooth much more to avoid false signals but with more lag.

This technical indicator should be used with other ones to confirm its information.

//PRC_Volatility Cycle | indicator

//02.12.2016

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

//converted and adapted from Metatrader4 version

InpBandsPeriod=18 // Period

Smooth=2 // Smoothness

StdDev = std[InpBandsPeriod](close)

highindex = highest[InpBandsPeriod](StdDev)[1]

lowindex = lowest[InpBandsPeriod](StdDev)[1]

if barindex>InpBandsPeriod then

VolDer = (StdDev-highindex)/(highindex-lowindex)

VolSmooth = average[Smooth](VolDer)

if VolSmooth>0 then

VolSmooth = 0

elsif VolSmooth<-1.0 then

VolSmooth = -1.0

endif

endif

RETURN VolSmooth as "Volatility Cycle"

Download

Filename:

PRC_Volatility-Cycle.itf

Downloads:

321

Legend

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...